That being said, all you need to know is two things;

ARM's and Negative Amortization Loans.

We're all familiar with ARM's. Originally intended for people who KNEW they were only going to live in a place for 3-5 years, these loans were a great way for them to build up equity in a house and take advantage of lower, short term interest rates.

Of course, ARM's started getting abused when people who shouldn't have been loaned money bought houses they couldn't afford using ARM's.

They are paying for it now with WSJP and short term interest rates at 8%+.

But my favorite was something that I thought shouldn't have existed.

You know, there are things that just SHOULD NOT EXIST.

Like genetically engineered mosquitos that carry AIDS. That's a bad idea.

Or dance shoes with glass soles. That's a bad idea.

Or surgical gloves laced with Ebola. That's a bad idea.

Or music that is repetitive with no lyrical component, talent or creativity, ie-rap. That's a bad idea.

Now common sense would dictate to most industries that you would not develop a product that would harm the potential customer. But what if your a mortgage banker with few moral scrupples. Everybody with good credit already has a loan. People with marginal credit already have an ARM, leaving only folk with the crappiest of credit. How do you get them a loan and your precious 1% commish?

Enter in the negative amortization loan or the "reverse amortization loan."

Here's a loan where you are charged interest, but you are so unable to afford the house, you can't even pay the INTEREST on the loan. But that's OK, BECUASE THAT'S THE IDEA OF A NEGATIVE AMORTIZATION LOAN! You pay only PART of the interest and the remaining balance of interest is ADDED to your principal balance on the mortgage. Thus you never actually pay down your mortgage balance, it only GOES UP.

Sudden rap doesn't sound half bad.

What I'm failing to grasp is why would any bank or financial institution push such a product? The only way I can see it, is if they are predatory and fully intend on collateralizing the house when (inevitably) the poor schmoe that was stupid enough to get a reverse mortgage can no longer afford the PARTIAL interest payments.

Of course, that's just how it affects the few unfortunate souls that engage in this sort of financing.

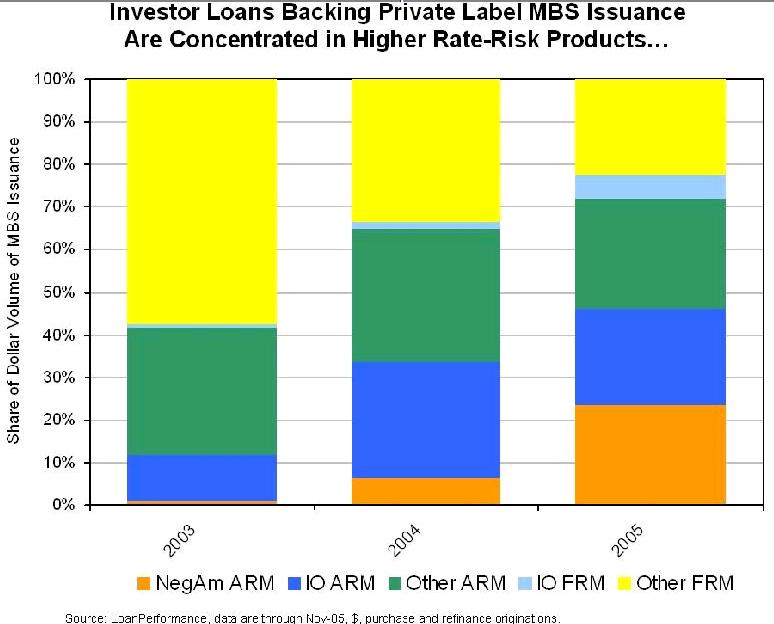

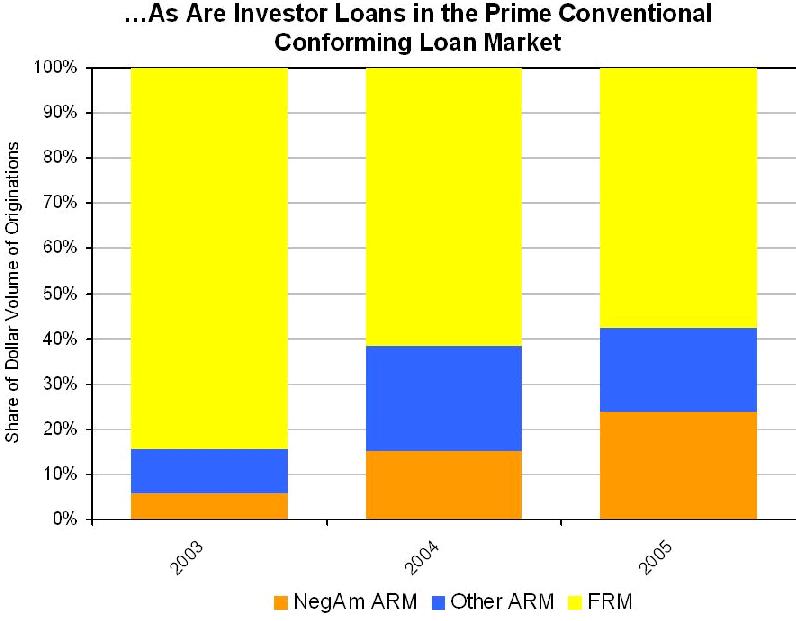

Unfortunately there are not so "few" unfortunate souls as ARM's and, worse still, negative amortization loans are becoming more and more common. Common enough to the point they no doubt are having an affect on their entire housing market (namely a housing bubble). Thus when 25% of the loans hitting the market in 2005 are negative amortization loans and an additional 23% are interest only loans, this money that should not have been given to people floods the housing market, artificially driving up prices. Artifically I say, because once interest rates go up (which they are), these people will quickly leave the market as they cannot finance the loan, flooding the market with housing that frankly, nobody really needs, and prices will drop to normal levels.

The question is whether this decrease or even temporary halt in housing prices will destroy the "wealth effect" that has prompted American consumers to spend more than they make via the Home Equity Loan, and has been one of the engines of the economy's growth in the past 5 years.

I smell a minor recession coming on.

No comments:

Post a Comment